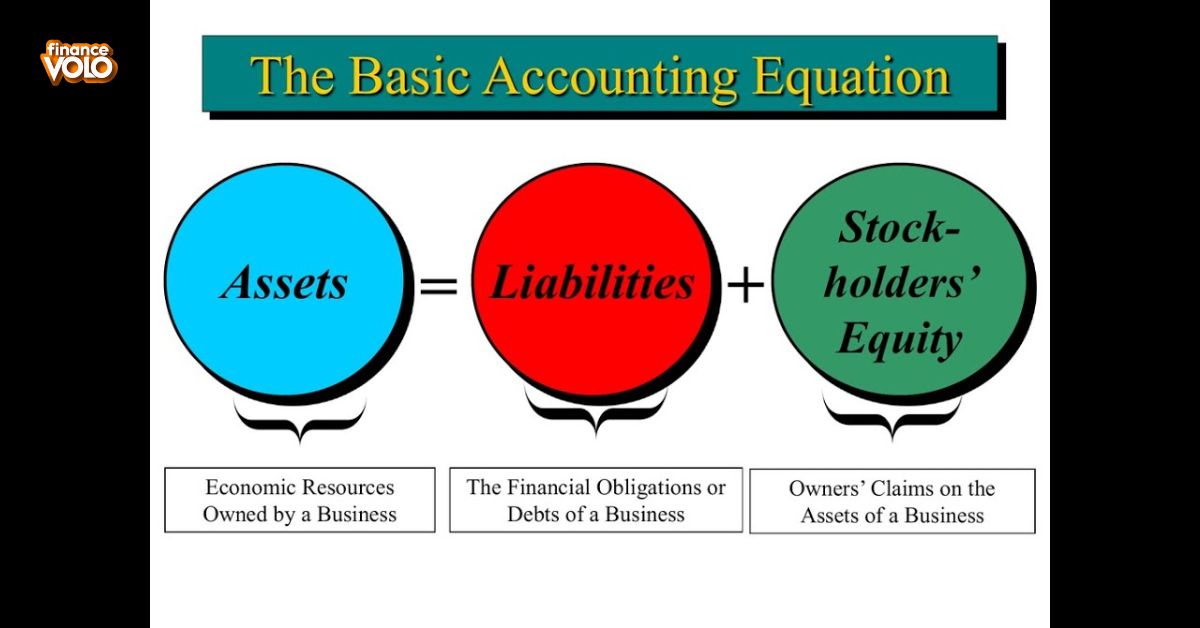

The accounting equation represents the fundamental principle of accounting: Assets equal Liabilities plus Equity. It illustrates the relationship between a company’s resources, debts, and ownership interests. Enter the accounting equation, the backbone of financial management. It’s a simple yet powerful concept that states.

Assets equal Liabilities plus Equity. In essence, it shows how a company’s resources are funded whether through debts or owner contributions. Understanding this equation is key to unraveling the mysteries of financial statements and decision-making in the business world.

What Are the Key Components in the Accounting Equation?

The accounting equation comprises three essential components: assets, liabilities, and equity. Assets represent what a company owns or controls, including cash, inventory, and property. Liabilities encompass the debts and obligations owed by the company to external parties, such as loans and accounts payable. Equity represents the ownership interest in the company, reflecting the residual claim of its owners after deducting liabilities from assets. Below are examples of items listed on the balance sheet.

Assets

Assets are resources owned by a company, such as cash, inventory, and property. They represent the economic value that a business controls and can use to generate revenue. In accounting, assets are recorded on the balance sheet and are essential for assessing a company’s financial health.

Liabilities

Liabilities are obligations or debts that a company owes to external parties, such as creditors or suppliers. They represent claims against a company’s assets and must be settled in the future, typically through the transfer of economic resources. Examples of liabilities include loans, accounts payable, and accrued expenses.

Shareholders’ Equity

Shareholders’ equity represents the residual interest in the assets of a company after deducting liabilities. It reflects the ownership stake of shareholders in the company’s net assets. Essentially, it’s what shareholders would receive if all assets were liquidated and all debts paid off.

What Is the Double-Entry Accounting System?

The double-entry accounting system is a method used by businesses to record financial transactions. It operates on the principle that every transaction affects at least two accounts, with one debit entry and one credit entry. This system ensures that the accounting equation (Assets = Liabilities + Equity) remains balanced and accurate.

Each transaction is recorded in two separate accounts: one account is debited to reflect the increase or decrease in its value, while another account is credited to show the corresponding change. By adhering to this system, businesses can maintain detailed records of their financial activities, facilitating accurate financial reporting and analysis.

Accounting Equation in Practice

In practice, the accounting equation serves as the foundation for maintaining accurate financial records. It guides businesses in recording transactions and preparing financial statements. By ensuring that assets always equal the sum of liabilities and equity, it helps maintain the integrity of a company’s financial data.

The accounting equation aids in financial analysis and decision-making. It provides insights into a company’s financial position and performance over time. By monitoring changes in assets, liabilities, and equity, businesses can assess their liquidity, solvency, and overall financial health.

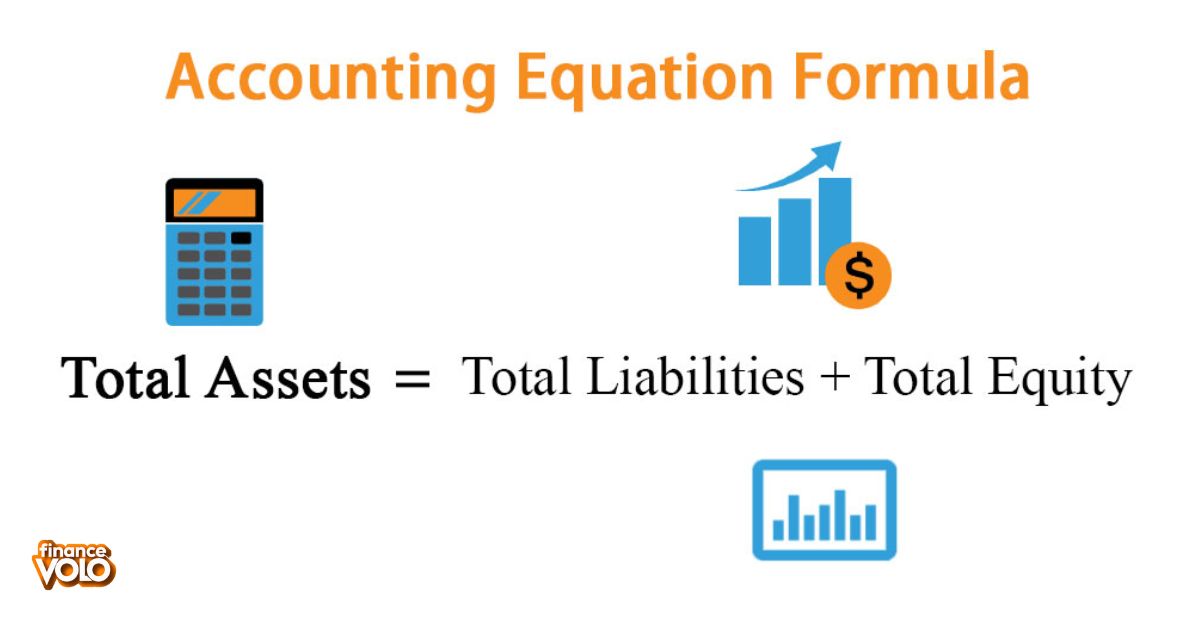

Accounting equation formula and calculation

The accounting equation, Assets = Liabilities + Equity, is the cornerstone of double-entry bookkeeping. It ensures that a company’s resources are always balanced against its debts and owner’s claims. Calculating it involves tallying up all assets and then summing up liabilities and equity to ensure equilibrium.

To calculate the accounting equation, start with listing all assets like cash, inventory, and equipment. Then, sum up all liabilities, such as loans and accounts payable, along with equity, including contributed capital and retained earnings. Finally, confirm that the total assets match the sum of liabilities and equity, ensuring accuracy in financial reporting.

Limits of the accounting equation

The accounting equation, while foundational, has its limitations. Firstly, it assumes that all assets can be reliably valued and measured, which might not always be the case, especially with intangible assets like goodwill. it doesn’t account for changes in market values over time, potentially leading to discrepancies between book value and true economic value.

The equation may overlook certain economic events and transactions, such as off-balance sheet items or contingent liabilities, which can impact a company’s financial health. It doesn’t consider factors like inflation or changes in purchasing power, affecting the accuracy of financial reporting over extended periods.

What Is a real-World example of the Accounting Equation?

In everyday life, consider buying a house using a mortgage. Initially, the house becomes an asset, increasing one side of the accounting equation. However, since a mortgage is a liability, it also contributes to the equation’s balance by increasing the liabilities side. So, Assets (the house) = Liabilities (the mortgage) + Equity (the owner’s stake in the house).

When a business purchases inventory on credit, it increases assets (inventory) and liabilities (accounts payable), maintaining the balance of the accounting equation. Thus, the equation reflects the financial reality of transactions, providing a clear picture of a company’s financial position.

Why Is the accounting equation important?

The accounting equation is crucial because it serves as the foundation for double entry bookkeeping, ensuring accuracy in financial records. By balancing assets with liabilities and equity, it helps maintain the integrity of financial statements, aiding in decision-making and financial analysis.

The equation provides insight into a company’s financial health and stability. It allows stakeholders to assess solvency, liquidity, and overall performance by understanding how resources are financed and utilized. Ultimately, it guides strategic planning, investment decisions, and regulatory compliance, making it indispensable in the world of finance.

What are the three elements of the accounting equation?

The accounting equation comprises three vital components assets, liabilities, and equity. Assets encompass everything a company owns or controls, from cash and inventory to property and investments. Liabilities represent the company’s debts and obligations, while equity reflects the owners’ stake in the business after liabilities are deducted from assets.

What is an asset in the accounting equation?

An asset in the accounting equation is anything of value that a company owns or controls. It includes tangible items like cash, inventory, and property, as well as intangible assets like patents and trademarks. Assets are vital as they represent the resources available for a company to use in its operations or to generate future benefits.

What Is a Liability in the Accounting equation?

A liability in the accounting equation represents a company’s obligations or debts. It includes amounts owed to creditors, such as loans, accounts payable, and accrued expenses. Liabilities are essential for understanding a company’s financial obligations and overall financial health.

What is shareholders’ equity in the accounting equation?

Shareholders’ equity in the accounting equation represents the ownership interest of shareholders in a company’s assets. It’s calculated by subtracting total liabilities from total assets, indicating the residual value available to shareholders. Essentially, it reflects the portion of a company’s assets that shareholders own outright.

Related Post: What Is Accounting?

Examples of accounting equation transactions

Here are some examples of accounting equation transactions:

Buy Fixed Assets on Credit

Buying fixed assets on credit involves acquiring long-term assets such as machinery or equipment with a promise to pay later. This method allows businesses to invest in essential assets while spreading out the cost over time. However, it increases liabilities initially until the debt is repaid.

Buy Inventory on Credit

Buying inventory on credit involves obtaining goods from suppliers with the promise of payment at a later date. It allows businesses to acquire necessary inventory without immediate cash outlay, aiding cash flow management. However, it also increases liabilities, as the company owes money to the supplier until the credit terms are fulfilled.

Pay Dividends

Paying dividends refers to distributing a portion of a company’s profits to its shareholders. It’s a way for companies to reward shareholders for their investment. Dividends are typically paid in cash but can also be issued as additional shares of stock.

Pay Rent

Paying rent involves regularly providing a specified amount of money to a landlord or property owner in exchange for the use of a space. It’s a common practice for individuals and businesses to secure housing or commercial premises without the financial commitment of ownership. Rent payments typically cover the agreed-upon period and contribute to the landlord’s income for maintaining the property.

Pay Supplier Invoices

Paying supplier invoices involves settling bills owed for goods or services received. It’s a crucial aspect of maintaining positive vendor relationships and ensuring continuity in business operations. Timely payment of invoices helps avoid late fees and demonstrates reliability in fulfilling financial obligations.

Sell Goods on Credit

Paying supplier invoices involves settling bills owed for goods or services received. It’s a crucial aspect of maintaining positive vendor relationships and ensuring continuity in business operations. Timely payment of invoices helps avoid late fees and demonstrates reliability in fulfilling financial obligations.

Sell Stock

Selling stock involves offering shares of ownership in a company to investors in exchange for capital. It’s a common method for companies to raise funds for expansion or operations. Investors who purchase stock become partial owners and may benefit from dividends and capital appreciation.

Related Post: How To Get Into Investment Banking

Additional accounting equation issues

Additional accounting equation issues may involve complex transactions, such as stock splits or revaluations, which require careful consideration to maintain balance. More discussed about additional accounting equation issues in below

Rounding error

A rounding error occurs when a calculation is rounded to a certain number of decimal places or significant figures, leading to a slight discrepancy from the precise value. It can occur in various mathematical operations, especially when dealing with fractions or decimals. Rounding errors are often insignificant but can accumulate over multiple calculations, potentially affecting the accuracy of financial or scientific analyses.

Unbalanced starting numbers

Unbalanced starting numbers occur when the initial figures in accounting records do not align with the accounting equation. This imbalance can lead to inaccuracies in financial statements and misrepresentation of a company’s financial position. Correcting unbalanced starting numbers is crucial for maintaining the integrity and accuracy of financial reporting.

Unbalanced transactions

Unbalanced transactions occur when the accounting equation is not satisfied, leading to discrepancies in financial records. This imbalance can arise from errors in recording or omitting certain transactions. Resolving unbalanced transactions is crucial for maintaining accurate financial statements and ensuring the integrity of accounting data.

Frequently Asked Questions

What is the accounting equation?

The accounting equation is a fundamental principle in accounting that states: Assets equal Liabilities plus Equity.

Why is the accounting equation important?

It provides a framework for understanding how a company’s resources are financed and how financial transactions affect its overall financial position.

How does the accounting equation balance?

The equation balances because every transaction affects at least two elements: assets and either liabilities or equity, ensuring that the equation remains in equilibrium.

Can you give a real-world example of the accounting equation?

Sure, when a person buys a car using a loan, the car becomes an asset, the loan becomes a liability, and the owner’s equity represents their stake in the car.

What happens if the accounting equation doesn’t balance?

If the equation doesn’t balance, it indicates errors in recording transactions or incomplete data, which must be identified and corrected to ensure accurate financial reporting.

Final Words

The accounting equation serves as the foundation of financial accounting, stating that Assets equal Liabilities plus Equity. It provides a clear framework for understanding how a company’s resources are financed and how transactions impact its financial position. By balancing assets against liabilities and equity, it ensures that every financial transaction is accurately recorded.

In practical terms, the equation is like a scale, with assets on one side and liabilities plus equity on the other. For instance, when a business takes out a loan to purchase equipment, the equipment becomes an asset while the loan becomes a liability, maintaining the equation’s balance. Understanding and applying the accounting equation is essential for businesses to track their financial health and make informed decisions about their operations.